Deal Summary

During the depths of the recession, billionaire investor Carl Icahn submitted the one and only qualified bid in a Miami bankruptcy court to acquire the land and improvements of the former FontaineBleau Las Vegas, for $150,000,000. The price Icahn paid for the approximately 70% completed megaresort and tallest hotel tower in Nevada amounted to less than 10% of what had already been invested in constructing the improvements. In 2016, six years after acquiring the property, Carl Icahn is reported to be close to finalizing a sale of the property for an estimated $650,000,000. By reviewing the complete story and analyzing Icahn’s investment, we’ll try to gain a deeper understanding of real estate investing, and walk away with some lessons which will help us in making better investing decisions in our own lives.

Background of the Fontainebleau Las Vegas Development (Before bankruptcy)

The Mid-2000s were an exciting time in Las Vegas, when there seemed to be abundant growth potential for the tourism industry in the country’s entertainment capital. From 1982-2005, the number of annual visitors to Las Vegas had increased from about 11.5 million to over 38.5 million, the culmination of 33 consecutive years of consistently increasing visitor traffic. Furthermore, by 2005, lodging occupancy in Las Vegas had climbed to a new recent high, with an annual average of 89% occupancy of the city’s hotel rooms. Las Vegas had cemented its position as the preferred international destination for conventions, and the life-blood of the Las Vegas strip, gaming revenues, were in the midst of increasing 10% year-over-year for two straight years and rapidly approaching $10 Billion annually. By all metrics, the Las Vegas Strip seemed primed and ready for another multi-billion dollar casino project.

Meanwhile, in early 2005, Florida-based developer Turnberry Associates, specializing in developing hotels, high-end Condominiums, and office buildings, had just acquired the famed and historic Fontainebleau Miami Beach. Originally constructed during the 1950s, the then 920-room resort was arguably the most luxurious and historic hotel in South Florida, comparable in status to the Beverly Hills Hotel in Beverly Hills, CA and the Hotel Del Coronado in Coronado, CA. Immediately after acquiring Fontainebleau Miami Beach, Turnberry Associates CEO, Jeffrey Soffer, began planning a billion dollar renovation and expansion of the Fontainebleau Miami Beach, as well as the development of a new sister property on the Las Vegas Strip. Keeping in line with the grand ambitions of the Las Vegas market, Soffer envisioned the tallest hotel tower in Nevada. The proposed resort was planned to include almost 4,000 rooms, 100,000 square feet of casino space, a 3,300-seat performing arts theater, 180,000 square feet of retail space, and 400,000 square feet of convention space – all situated on 24.5 acres of prime land on the up-and-coming north end of the Las Vegas Strip.

Satellite map of the Las Vegas Strip labeling the site of the former Fontainebleau Las Vegas

Aerial View of Immediate area of former Fontainebleau Hotel

Birds Eye View of Fontainebleau Las Vegas

Birds Eye View of Fontainebleau Miami Beach

At the time of Turnberry’s acquisition of Fontainebleau Miami Beach, Turnberry already owned the 24.5 acres of vacant land on which the Fontainebleau Las Vegas was proposed to be built. About 5 years earlier, in 2001, Turnberry Associates developed the adjacent parcel immediately behind the 24.5 acres into four high-rise luxury condominium buildings, each of which are 40 floors, and are still the tallest residential condominium buildings in Nevada. Considering Turnberry’s recent acquisition of Fontainebleau Miami Beach in 2005, and it’s ownership of 24.5 acres of prime land fronting Las Vegas Boulevard adjacent to its already existing flagship condominium development, Turnberry Associates finally had the missing piece of the puzzle: an internationally recognized hotel brand which could justify building a multi-billion dollar hotel on the Las Vegas Strip.

Within months of acquiring Fontainebleau Miami Beach, Turnberry Associates announced plans to build Fontainebleau Las Vegas as a sister property to its historic, flagship hotel in Miami Beach. Along with the announcement, Turnberry Associates appointed Ex-Mandalay Bay Chief Financial Officer, Glenn Schaeffer, to head the development of the Fontainebleau Las Vegas as well as the billion dollar renovation and expansion of Fontainebleau Miami Beach. The official groundbreaking date of Fontainebleau Las Vegas was April 30, 2007 and the tower topped out at its full height of 735 feet during November 2008.

Rendering of Fontainebleau Las Vegas

About two years into the construction process and after about $2 billion had already been spent on constructing the improvements, during mid-2009 the project’s lender, Bank of America, refused to fund the remaining $800 million of construction loans which Turnberry needed in order to complete construction. Without anywhere else to turn, during June 2009 the Fontainebleau Las Vegas filed Chapter 11 bankruptcy to relieve itself of debts and obligations. Without warning, the ambitious project was stalled and left in its unfinished state as a stark reminder that not everything is possible, even in the capital of excess, extravagance and seemingly endless possibilities.

Photo of partially-completed Fontainebleau Las Vegas

Bankruptcy (June 2009 – February 2010)

During mid 2009, the bankruptcy sale was marketed to 157 potential interested parties. Out of those 157 parties, eight signed confidentiality agreements which would provide the interested parties with access to review specific and detailed information about the property. At the Miami bankruptcy court, the judge reviewed three offers and immediately disqualified two of the offers which didn’t adhere to the rules and terms of the auction. This left just one offer at a price of $150,000,000, which was submitted by contrarian investor Carl Icahn.

Icahn’s purchase price amounted to a bit over $6 million/acre, a deep discount to the $34 million/acre that parcels fit for hotel development were selling for just a few years earlier. For example, just three years earlier, in May 2007, Phil Ruffin sold the 36-acre parcel which then housed the New Frontier Hotel for $1.2 billion or $34 million/acre. The steep drop in Strip land values is even more extreme when the improvements on each of the properties are taken into account. The buyers of the New Frontier Hotel spent millions of dollars to wind down the hotel operations and to demolish the existing hotel soon after acquiring it. The Fontainebleau hotel, on the other hand, included millions of dollars of brand new furniture and an approximately 70% completed resort, into which $2 billion had already been invested.

About Carl Icahn

Over the past 30 years, Carl Icahn has repeatedly demonstrated his shrewdness by noticing untapped potential and long-term value in public companies and and private assets. In the 1980s, he became a prominent figure on Wall Street by accumulating significant ownership stakes in public companies, and then using his significant ownership stakes to influence the companies to use cash reserves to buy back company stock, cut costs, sell a subsidiary, or to make other strategic moves. Often times, his efforts resulted in substantial increases in the value of the companies he was targeting. Other times, defensive company leadership fought off Icahn’s involvement, sometimes going so far as using company funds to pay off Icahn to abandon his efforts, a process that came to be known as “greenmail,” a play off of the word “blackmail.” Expectedly, Carl Icahn is a business figure who has made many enemies during his investing career. However, almost all can agree of his impressive track record of recognizing opportunities in the market.

Ownership Process (2010-2016)

Icahn’s ownership of the Fontainebleau was uneventful, seemingly prioritizing expense minimization above all else. Within a few months of acquiring the property, Icahn auctioned off all of the building’s furniture (reportedly including carpeting, wallpaper, mattresses, wall safes, chairs, bed frames, bedside tables, couches, and more). Much of the furniture was acquired by the Plaza Hotel in Downtown Las Vegas, which was able to complete a thorough renovation of its 1,137 hotel rooms which has been described by Plaza Hotel executives as “pennies on the dollar” and “lucky,” and which played a significant role in a renovation which executives estimate will double the average daily rates for the Plaza Hotel. Based on the quoted $2 million which the Plaza Hotel spent on furnishings during their renovation, Icahn likely netted approximately $5 million from auctioning off all of the personal property included in his acquisition of the former Fontainebleau Las Vegas.

Rendering of the proposed Fontainebleau Las Vegas hotel rooms

The second significant cost during Icahn’s ownership occurred during 2015, when an existing deadline was approaching for Icahn to make infrastructure improvements to the sidewalk, road, and landscaping surrounding the site of the former Fontainebleau Hotel. Finally having some negotiating leverage over Icahn, the City was able to pressure Icahn into installing a cloth cover over the lower 100 feet of the building, which the City thought to be a major eyesore to pedestrians and traffic traveling along Las Vegas Blvd. Based on similar covers previously installed in the last few years, estimated costs for the installation are $1 million, a small fraction of the the likely costs of the looming infrastructure improvements.

Marketing and sale of the former Fontainebleau (Expected to be finalized in late 2016)

In November 2015, Icahn enlisted the services of CBRE to market the former Fontainebleau site and improvements for an estimated $650 Million. During mid-2016, multiple local news outlets reported that a sale of the former Fontainebleau site is expected to close in late 2016 at a price at or near the estimated asking price.

Jon Knott, executive vice president at CBRE, explains that the new owner will most likely complete construction on the existing building because it would be cost prohibitive to demolish the existing structure and build a brand new resort. Over ten years have passed since the days when anything less than boundless ambition was the only unforgivable sin in Sin City. Ten years later, the days of paying $34 million/acre (plus demolition costs) plus billions of additional dollars to build over-the-top resorts still seem to be a distant memory from the early 2000s.

Calculating the Return on Icahn’s Investment

How profitable was Carl Icahn’s investment in the former Fontainebleau? Let’s take a look at estimated returns that Icahn may have earned from this investment. Specifically, we’ll be focusing on estimating each year’s cash flows in order to calculate the internal rate of return for both a cash purchase and a financed purchase. The assumptions for the financial projections are as follows:

- Purchase Price: $150,000,000

- Acquisition Costs (Due Diligence, Closing costs, Legal Fees, etc.): $2,500,000

- Carrying costs (property taxes, insurance, maintenance/repairs, etc): $5 Million/year for years 1-7

- Proceeds from sale of furniture and personal property: $3 Million in Year 1

- Other Expenses: $1 Million spent in Year 6 to cover the lower 100 feet of the building

- Sale Price: $625,000,000

- Sale Costs (commission, legal fees, potential discount): $25,000,000

- Loan assumptions for financed purchase:

- 70% Loan-to-Value

- 5% interest-only payments

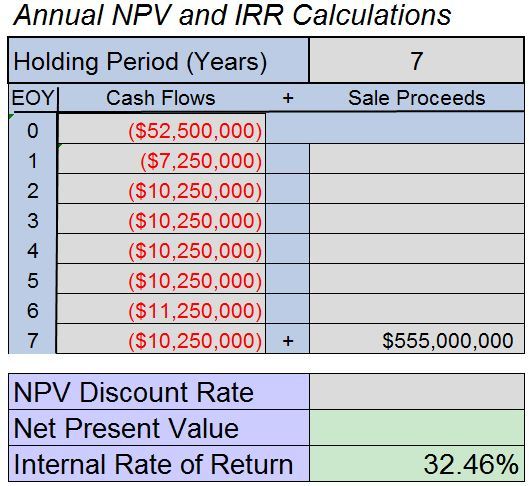

Estimated cash flows and IRR calculation based on all-cash purchase

Estimated cash flows and IRR calculation based on a financed purchase

Based on the above calculations, Icahn earned a healthy, respectable return from his investment in the former Fontainebleau Las Vegas. Considering the huge sum of money invested (earning ~20% on a $150 Million purchase is much more difficult than earning 20% on a $1 Million purchase), considering Icahn’s relatively passive ownership (lack of major time, capital, and resources spent on improving the property), and also considering the 7 year holding period (% annual returns naturally become lower as the holding period increases), Icahn’s return seems even more attractive.

Another often overlooked area of returns is the expense write-offs which Icahn probably took advantage of during his 7-year ownership of the former Fontainebleau Las Vegas. One of the main benefits available to real estate investors is being able to deduct a substantial amount of expenses which can sometimes serve to entirely offset taxes that the investor would otherwise be obligated to pay. Considering that the former Fontainebleau site wasn’t producing any income during the 7-year holding period, virtually all expenses (including cash and non-cash expenses) could have been deducted from Icahn’s total income, thereby providing significant tax savings. To demonstrate the significance of the potential tax savings, let’s take a look at the Year-2 potential expense write-offs for a leveraged purchase of Fontainebleau:

- Interest Expense:

- Loan Amount * Interest Rate = Interest Expense

- $105 Million * 5% = $5,250,000

- Estimated Holding Costs

- Property taxes + Insurance + Repairs/Maintenance + Other Expenses):

- Estimated at $5,000,000

- Depreciation Expense:

- Improvement allocation * (Purchase Price + Acquisition Costs) / 39 yrs Depreciable Life

- Estimated 75% * ($150 Million + $2.5 Million) / 39

- Estimated at $2,933,000

- Total Annual Expense write-offs: $13,183,000

Based on the above estimated tax-write offs, Icahn could have written off over $13 Million of expenses during each of the seven years of ownership. Assuming a 35% income tax rate, these expenses would result in an annual tax savings of over $4,500,000. Click here to learn more about tax deductions available to real estate investors.

Perhaps one of the greatest real estate tax benefits is the ability for investors to do a 1031 exchange (also called a like-kind exchange) by indefinitely deferring the gains on one investment as long as the proceeds from a real estate sale are reinvested into another investment property. There are many rules and intricacies to completing a successful 1031 exchange, but if Icahn were to complete a 1031 exchange simultaneously with the sale of the Fontainebleau site, there could be significantly more tax benefits. Click here for a background and introduction into 1031 exchanges.

Lessons and Takeaways

Now, let’s go through some lessons and takeaways from Icahn’s investment in the former Fontainbleau hotel.

Lesson 1: Understand the risks/challenges of ground-up development. Renovations and expansions of existing properties may provide similar returns with less risk.

Simply put, developers of new projects expose themselves to many risks which investors acquiring existing buildings aren’t exposed to. These risks are amplified in the both the cyclical hotel and casino businesses, as well as the notoriously cyclical Las Vegas real estate market.

Turnberry Associates was and still is an extremely experienced developer who was better equipped than almost anyone to build a $3 billion casino resort in Las Vegas. In fact, within a couple of blocks of the Fontainebleau Las Vegas site, Turnberry Associates had already developed thousands of luxury condominiums, including the tallest and largest residential condominium complex in Nevada. Furthermore, Turnberry Associates owned a well-regarded hotel brand and the Fontainebleau Las Vegas project was being spearheaded by an experienced team including over 30 former Mandalay Bay high-level executives who had just recently come off of Mandalay Bay’s sale to MGM in one of the many multi-billion dollar transactions during the early 2000s.

The issues encountered by Turnberry Associates while developing Fontainebleau can almost completely be attributed to the state of the economy and the cyclical nature of the real estate market. In Las Vegas, where the local economy is heavily dependent on tourism and entertainment, a nationwide recession can significantly influence the local economy and property values, as did occur during the Great Recession. Within a few months, the number of annual visitors to Las Vegas and gambling revenues were both plummeting, and several multi-billion dollar, under-construction resorts were on the brink of foreclosure. One such project was the Cosmopolitan, whose owner defaulted on over $760 Million of loans in 2008 while the property was under construction. Just a few months later, the developers of the Cosmopolitan relinquished possession to Deutsche Bank, the property’s lender.

However, Fontainebleau Las Vegas was a different story. Unlike the developer of the Cosmopolitan, Turnberry Associates remained confident and steadfast in their plans to construct the hotel, even in light of signs of a deep recession in 2008 and 2009. By Mid-2009, Fontainebleau was approximately 70% complete with over $2 Billion already spent on building most of the resort. In Mid-2009, the project’s main lender, Bank of America, abruptly refused to fund the remaining $800 million it had originally intended to. Jeffrey Soffer, CEO of Turnberry Associates, did everything in his power to coerce Bank of America into fulfilling its lending commitment, including going so far as to having the contractor of the project (a company controlled by Jeffrey Soffer) sue the developer of the project (another company controlled by Jeffrey Soffer), in a roundabout attempt into forcing Bank of America to fork up the remaining funds. Bank of America ultimately refused to lend any additional funds and the Fontainebleau Las Vegas declared Chapter 11 bankruptcy shortly thereafter.

Does Bank of America deserve all of the blame for withdrawing its commitment to lend the remaining $800 million required for Fontainebleau’s completion? Probably not. If we can draw any parallels between the Cosmopolitan and the Fontainebleau Las Vegas, then Bank of America may have been wise in cutting off funding for the remaining Fontainebleau construction work. In 2008, when the developer of the Cosmopolitan, Ian Eichner, defaulted on $760 Million of loans to Deutsche Bank, Deutsche Bank took over the property and invested over $3 Billion of additional funds to complete the hotel in time for its grand opening in 2010. Although the Cosmopolitan has been highly popular, the hotel never reported a quarterly a profit until it was sold to private equity firm Blackstone in 2014 for $1.73 billion, less than half of what Deutsche Bank invested in constructing the hotel. It’s hard to tell whether Fontainebleau would have faced a similarly unprofitable fate as the Cosmopolitan, but with its funding cut off, it never even had its chance.

Looking back, how could have this failure have been avoided? To understand a different strategy, all we have to do is take a look at the Fontainebleau Las Vegas’ sister property in Miami Beach. In 2005, the Fontainebleau Miami Beach was a successfully operating 920-room hotel in Miami Beach. Noticing untapped potential, in 2005 the new owner, Turnberry Associates, announced a billion-dollar renovation and expansion to add numerous amenities and almost double the number of rooms at the hotel. The renovation and expansion were completed before the end of 2008, while the existing hotel was operating and generating revenue. Unlike the Fontainebleau Las Vegas, the relatively modest renovation and expansion of the Fontainebleau Miami Beach was completed in a shorter timeframe, built upon a time-tested and proven 50-year old business and location, and was generating revenue throughout the entire renovation and expansion process.

Before real estate investors are entranced by the excitement of building a new building, they should think analytically about the risks and rewards of ground-up development, relative to the risks and rewards of acquiring existing buildings . Although a 25% IRR may be sufficient for an investor planning on acquiring, renovating, and selling an existing building, the same investor should not settle for a similar 25% IRR for a riskier ground-up development.

Lesson 2: If you’re buying a property without income and holding it for more than a couple years, the value appreciation must be very large in order for an investor to earn a decent annual return. If the value appreciation isn’t very large or if the holding timeframe isn’t relatively short (1-2 years), most investors would likely be better off acquiring an income producing asset.

In acquiring the former Fontainebleau Las Vegas, Icahn’s primary opportunity cost was $152,500,000 which could have been invested in high yield, income-producing real estate or other income-producing assets. Not only did Icahn not receive any cash flows for six years, he actually had to spend tens of millions of dollars out-of-pocket to meet the property’s expenses.

Although the huge appreciation over the 7-year holding period still made the return attractive, the huge appreciation in the property value was definitely not a sure thing. And this investment could have easily turned from a decent one to a terrible one if the economy remained in an extended recession and the value of the former Fontainebleau didn’t increase. My opinion is that Icahn expected the property value to appreciate much more than it actually did or to appreciate to its current value in a much shorter timeframe, thereby earning a much higher annual return.

Another possible investment strategy would be to acquire a strong, cash-flowing asset producing a 10% cap rate. Such investments were widely available during the depths of recession, and could have led to a much safer, more predictable outcome. If this alternative property was financed with a 20% down payment and 5% interest, the investor’s cash-on-cash return would be 25% on just the cash flow. If the alternative property’s cash flow gradually increased as the economy improved and valuation cap rates decreased from 10% to 8%, the investor could have multiplied their investment many times over and recouped their initial investment in 2-3 years rather than waiting 7 years until the sale of the property.

A clear example of this strategy can be witnessed through Phil Ruffin’s $775 Million acquisition of the Treasure Island Resort from MGM in a deal announced in mid-2008. After selling the 36-acre New Frontier hotel site to Elad Properties for $1.2 Billion in 2007, Ruffin acquired the approximately 15 year-old, 2,885 room Treasure Island Resort and Casino which at the time had an EBITDA of $101 Million. Ruffin estimates that a resort and casino like Treasure Island would cost about $2.8 billion to rebuild today.

As good of a deal as Icahn’s acquisition of Fontainebleau seems to be, I think Ruffin’s sale of the dilapidated New Frontier, and subsequent acquisition of the Treasure Island was a much better investment. Since Ruffin’s acquisition of the Treasure Island, he has acquired the Primm Valley Casino and submitted a $1.3 Billion offer on the real estate of The Mirage (management and operations not included), which was declined by MGM in 2015.

Lesson 3: This deal shows how an investor can ride a wave of the real estate cycle, which can single handedly carry a deal to a huge profit even in the absence of any other work or improvements to a property.

Another lesson from Carl Icahn’s acquisition of the former Fontainebleau Las Vegas is the ideal timing of his acquisition, which presents a clear view of the true power of riding the wave of the real estate cycle. Icahn’s ownership was characterized by expense-minimization and patience. Therefore, any appreciation in the property value can be specifically attributed to the swings in the real estate cycle. Based on the below graph, Icahn acquired the former Fontainebleau Las Vegas in 2010 during Phase IV/Recession which was characterized by increasing lodging vacancy rates and the recent completions of the Wynn, Encore, Aria and Cosmopolitan. Now, Icahn looks poised to complete the sale of the former Fontainebleau in late 2016 during Phase II/Expansion which is characterized by declining vacancy rates and groundbreaking for new projects such as Resorts World Las Vegas, a 7,000-room mega resort and casino with completing expected in 2019.

The four quadrants of the real estate cycle

Lesson 4: Buying real estate below replacement cost. (Value Investing’s application to real estate investing)

Value Investing is an investment approach popularized by Benjamin Graham and Warren Buffet, where investors seek underpriced assets which are trading at a discount to intrinsic value, discount to value of a company’s equity, or at a low PE ratio. The discount at which the investment is acquired is called the margin of safety, because it provides a profit cushion which acts to safeguard the investor’s initial investment in case the investment loses some of its value. When applied to investing in securities, this investing approach has generated outsized returns for the likes of Warren Buffett.

One way to apply this investment philosophy to real estate is by acquiring real estate assets at a discount to replacement cost, or what it would cost to replace/rebuild the improvements on the property. For example, if an investor acquires a newly-built building at a deep discount for $1 Million, and that same building would cost $2 Million if an investor wanted to rebuild an identical building, then the investor acquiring a property for $1 Million may experience a margin of safety of about $1 Million. In Icahn’s acquisition of the former Fontainebleau Las Vegas, Icahn acquired building improvements which would cost about $2 Billion to rebuild as they stood in 2010. Obviously, a rational investor wouldn’t spend $2 Billion today to rebuild the existing improvements on the land, however there is still a significant amount of value, security and margin of safety due to the cost of the existing improvements on the site. Moreover, it was reported that during his holding period, a Chinese company offered Icahn $200 Million for the value of the scrap metal on the site of the former Fontainebleau Las Vegas.

Lesson 5: There can be major opportunities (and risks) in asset classes that are very cyclical and that have higher ownership responsibilities

Because of the relatively high fixed costs of running a hotel (as a proportion of total costs) and because of the hospitality industry’s extreme dependence on travel/tourism, the hospitality industry is very cyclical (Gambling revenue highly fluctuates, hotel occupancy and average daily rates in Vegas also highly fluctuate). When the economy is booming as it was in the mid 2000s, the hospitality industry outperformed most other sectors and surged to record profits and valuations. On the other hand, when the economy was struggling through the recession, the outlook for the hospitality and gambling industry plummeted much more than for other industries.

Within a year, tourism-related land valuations plummeted from $1.2 Billion for 34 acres of development land to the point where the Treasure Island, a 15-year old, 3,000 room hotel, with $100 MM of income, and an estimated replacement cost of $2.8 billion, was sold for $775 Million for.

Also, when there is a non-conventional asset, there is a much smaller pool of interested parties, and a much better opportunity to get a good deal. However, on the other hand if there’s an apartment building in Los Angeles, good luck buying it at much of a discount, regardless of the circumstances under which the property is being sold.

Lesson 6: Contrarian investing requires independent thinking, but can be rewarding

The old investing adage “buy low and sell high” is easier said than done. Generally speaking if an investor wants to buy low and sell high, an investor must usually invest when demand is relatively low, supply is relatively high, and market outlook is relatively pessimistic. When eventually selling the investment, the investor must usually follow through with the sale of the property when demand is relatively high, supply is relatively low, and market outlook is relatively optimistic. Not easy at all, but an investor with the intelligence and conviction to follow through with a contrarian investing approach can take advantage of the swings in the real estate cycle and earn outsized returns.

To understand how it felt to be an investor in 2009, it may help to read a few articles about the state of the Las Vegas market written during that time. A few articles published during that time contained facts, figures, and graphic imagery about rising unemployment, declining gambling revenues, declining occupancies and average daily rates for casinos, statistics about foreclosure rates in Las Vegas, which would cause any rational real estate investor to second-guess any contrarian investing approach it was planning on. Moreover, if an investor decided to gain reassurance in the fact that the big players in the Nevada Casino Industry were performing strongly, unfortunately that wasn’t an option either. MGM Mirage, one of the largest operators of resorts on the Las Vegas Strip, was struggling under $14 Billion of debt and had just sold off the Treasure Island at a fire sale price of $775 Million, about 25% of what it would cost to rebuild the 15-year old, 3,000-room resort and casino.

- Click here to read an article by The Guardian about the opening of the City Center complex in 2009

- Click here to read a 2008 article about the recession and its effect on Las Vegas

- Click here to read an 2009 article by CNN about the recession affecting Las Vegas

Contrarian investors have the conviction to acquire when the prevailing emotion is despair and to sell when the prevailing emotion is enthusiasm

Lesson 7: Minimizing total investment (including invested capital, time, and other resources) can potentially be a wise strategy for maintaining a high annual return on an investor’s resources

After Icahn’s acquisition of the former Fontainebleau it became immediately evident that Icahn planned to minimize any cash outlays for the Fontainebleau investment. Rather than completing construction of the hotel or storing new furniture that was included in his acquisition, he aggressively auctioned off all furniture, fixtures, and floorcoverings at amounts that were reported to be “pennies on the dollar.”

Icahn wisely predicted that any time, resources, and capital that would be expended on repairs, construction, storage, consultants, attorneys would not yield returns sufficient to justify the outlays. Contrast this approach to Deutsche Bank foreclosing on the Cosmopolitan hotel in 2008, and subsequently investing over $3 Billion to complete construction on the hotel, all to recoup less than half of its initial investment, after putting up with four consecutive years of operating losses after the hotel’s opening in 2010.

To demonstrate the effects of additional capital outlays on Icahn’s returns, consider that in order to maintain the 19.90% annual return in our above “all-cash purchase” IRR analysis, an additional $50 million of expenditures in Year 1 would need to yield an additional $150 Million at the time of sale in order to maintain the same 19.90% annual return. On the other hand, a $5 million cash receipt from sales of the Fontainebleau’s personal property in 2010 means that Icahn could now sell the property for $15 million less than originally anticipated at the end of 2016, and still earn the same 19.90% return.

Lesson 8: Cash is king and can open up many opportunities, such as buying distressed at the right times and buying bankruptcy sales, auctions, and other situations when financing isn’t available.

During 2009, there were likely many people who understood the opportunity present in the acquisition of the former Fontainebleau. However, there was just one offer deemed qualified by the Miami bankruptcy court, the $150 Million offer of Icahn. Although another investor, Penn National Gaming, had previously offered $300 Million for the site and improvements of the former Fontainebleau, Carl Icahn was able to acquire the former Fontainebleau for about half that price after the bankruptcy court reviewed all three of the offers. It’s fair to say that Icahn’s acquisition of the Fontainebleau would not have been possible if Icahn didn’t have the cash available to complete the purchase and hold the money-losing property for six years.

A liquid, cash investor is in a position to take advantage of quality properties being sold through unorthodox situations such as sheriffs sales, probate sales, REO’s, online auctions, bankruptcy auctions, when financing may be unavailable due to the situation of the property or due to the timeframe in which the investor needs to close on the acquisition.

Conclusion

One of the interesting things about real estate is that a good investment is subjective and depends on an investor’s financial situation, cost of capital, opportunity costs, investment time horizon, risk tolerance, market outlook and more. However, investors can always gain and learn from each other’s perspectives, strategies, successes and downfalls, which I hope we all did through the story and lessons from Icahn’s acquisition of the former Fontainebleau Las Vegas.

I’d appreciate hearing other perspectives, thoughts, and challenges to the above assumptions and lessons. Please feel free to comment on this post.

Sources:

http://www.vegastodayandtomorrow.com/fontainebleau.htm

http://vegasinc.com/business/tourism/2013/sep/02/rise-and-fall-land-strip/

http://www.vegastodayandtomorrow.com/fontainebleau.htm

http://www.reviewjournal.com/business/casinos-gaming/vacant-strip-land-frontier-site-remain-empty

http://www.reviewjournal.com/business/casinos-gaming/fontainebleau-owners-agree-cover-strip-eyesore

Click to access 1CB229D5-2D26-42C4-8A2E-884E067537F4_ERsupplemental.pdf