Deal Summary

In 1997, Douglas Emmett, a real estate investment company specializing in Class-A office buildings, acquired the Sherman Oaks Galleria for $51 million in an off-market transaction.

The Sherman Oaks Galleria, which consisted of approximately 1,000,000 square feet of retail and office space, became a cultural icon during the 1980s after being featured in movies such as Valley Girl and Fast Times at Ridgemont High. However, by the early 1990s the mall and its retailers struggled as the mall’s popularity subsided and customer traffic waned. To make matters worse, the 1994 Northridge Earthquake would accelerate the mall’s decline, which would continue its downward spiral until the mall’s 1997 off-market sale to Douglas Emmett.

Upon acquiring the property, Douglas Emmett hired Gensler Architects to envision and design a major renovation of the Sherman Oaks Galleria. The thorough $200 million repositioning strategy would include rebuilding, renovating, and repositioning the existing structures into what would be referred to as a lifestyle center, consisting of approximately 700,000 SF of office space supported by about 300,000 SF of retail space.

Following the renovation, rental rates at the Sherman Oaks Galleria doubled and occupancies climbed to above 99%. Today, the Sherman Oaks Galleria is a valued property in Douglas Emmett’s real estate investment trust (REIT) and has been awarded the TOBY (The Outstanding Building of the Year) award by BOMA (Building Owners and Managers Association International.)

A Cultural Icon: The Sherman Oaks Galleria during the 1980s

Opened in 1980, the Sherman Oaks Galleria would soon after become a cultural icon after the interior of the mall was featured in the movies Fast Times at Ridgemont High and Valley Girl, which were released in 1982 and 1983, respectively. The movie, Valley Girl, which is credited with the creation of the socioeconomic stereotype of the “Valley Girl,” became synonymous with the Sherman Oaks Galleria, which solidified the mall’s position as the epicenter of teenage mall culture.

However, during the early 1990s the general public’s endearment with the Valley Girl culture ended, and what once seemed hip and interesting, was now old and dull. Especially since malls are expected to provide entertainment and interesting experiences for visitors, coming across as old and dull is a grave sin. Despite the public’s disinterest, the Sherman Oaks Galleria likely could have treaded water for another decade or so, but a combination of additional factors during the 1990s would lead to an irreversible decline.

Pre-renovation photo of Sherman Oaks Galleria

The downfall: Robinson’s, May Company, and the 1994 Northridge Earthquake

The 1992 Merger of Robinson’s and May Company into Robinson’s-May

The first primary challenge the Sherman Oaks Galleria encountered was the 1992 merger of the malls two anchors, Robinson’s and May Company. Ever since the mall’s opening in 1980, a Robinson’s department store occupied the mall’s southern anchor space and a May Company department store occupied the mall’s northern anchor space. As a result of the merger, both anchor spaces were rebranded as Robinson’s-May department stores. Robinson’s-May’s northern anchor store would consist of the men’s and home department, and their southern anchor store would consist of a women’s and children’s department.

The mall’s two identically-branded anchor spaces likely didn’t arouse much of the general public’s enthusiasm and excitement. Presented with all of the San Fernando Valley’s shopping mall choices (Westfield Fashion Square, Northridge Fashion Center, and Westfield Topanga), there likely wasn’t much of a reason to visit the only mall with just one department store brand.

The 1994 Northridge Earthquake

In the early hours of January 17, 1994, a 6.7 magnitude earthquake rattled the San Fernando Valley, resulting in over 9,000 casualties and $40 billion in estimated property damage. The earthquake, which is often referred to as one of the costliest earthquakes in the country’s history, caused significant damage to both infrastructure and privately-owned buildings throughout the San Fernando Valley.

The Sherman Oaks Galleria emerged relatively undamaged by the earthquake, with the mall reopening just 11 days following the earthquake. However, the mall’s anchor tenant, Robinson’s-May, didn’t fully reopen its stores until more than four years following the earthquake. Much to the frustration of the mall’s ownership and the mall’s smaller retailers, the third floor of Robinson’s-May’s southern anchor store wouldn’t reopen until mid-1998. During the four year delay, most of the mall’s third-floor tenants vacated due to the insufficient traffic on the mall’s third floor.

Douglas Emmett acquires the Sherman Oaks Galleria for $51 Million

Three years into Robinson’s-May’s four-year reopening delay, Douglas Emmett acquired the Sherman Oaks Galleria for $51 million. The off-market transaction reflected a price-per-square-foot of just $51 for the mall’s 1,000,000 square feet of retail and office space. Although seemingly low, the $51 price PSF was justified. At the time of the mall’s 1997 sale, the mall’s income, occupancy, and reputation were in a steep decline, with average rents at $14.65/SF/year (about 50% below market) and occupancy at just 78.3%. Counteracting the mall’s downward spiral would require significant capital expenditures, several years of foregone rental income, and the successful implementation of a risky repositioning strategy.

Who’s to Blame? Douglas Emmett Sues Robinson’s-May, and Robinson’s-May Countersues

After Douglas Emmett’s 1997 acquisition, Douglas Emmett proceeded to clear out all of the mall’s tenants so that it could implement its redevelopment plans. By 1998, the mall’s occupancy had dwindled to approximately 40% and Douglas Emmett was now focused on forcing Robinson’s-May to vacate both the south and north anchor spaces of the mall.

To that end, in 1998 Douglas Emmett sued Robinson’s-May for its “unauthorized closure” of the third floor of its southern anchor store which lasted over four years, claiming that “virtually all the mall tenants located adjacent to the closed third floor … have vacated the mall due to lack of customer traffic.” Furthermore, Douglas Emmett charged Robinson’s-May with failing to adequately staff and stock its stores, thereby further contributing to the mall’s decline. Douglas Emmett’s goal in suing Robinson’s-May was to evict Robinson’s-May so that it could proceed with its redevelopment plans.

Robinson’s-May responded to the lawsuit by denying the charges and countersuing Douglas Emmett, charging that the mall’s owners “failed to operate [the mall] …. in a manner which attracts retail customers and tenants to the Galleria.” In its countersuit, Robinson’s-May was seeking compensation for money that Robinson’s-May had spent in developing, constructing, restoring, operating, and maintaining its two anchor stores.

Eventually, in January 1999 Douglas Emmett and Robinson’s-May settled the lawsuits at undisclosed terms, with Robinson’s-May winding down its operations and eventually vacating its anchor space by April 1, 1999. In less than 20 years, the Sherman Oaks Galleria had transitioned from a brand new mall, to a cultural icon, and finally into what would be described by the Los Angeles Times as a “moribund money-loser.”

Douglas Emmett embarks on a $200 million rebuilding and renovation of the Galleria

Considering that Douglas Emmett was one of the largest Class-A office building owners in Southern California, it was widely assumed that Douglas Emmett would incorporate a significant amount of Class-A office into its redevelopment of the Sherman Oaks Galleria.

However, Douglas Emmett had quite the challenge to overcome, at least in terms of the how the public perceived the mall. In a LA Times Article about the mall’s planned reopening, a local restaurant owner remarked, “Why didn’t they just let it die?” In another instance, the president of the anti-development Sherman Oaks Homeowners Association described the Galleria as a “white elephant,” pledging the notoriously anti-development association’s support for the mall’s redevelopment.

Douglas Emmett turned to Gensler’s Architect’s Santa Monica office to spearhead the design of the mall’s redevelopment. In an interview with ArchNewsNow.com, Andy Cohen, the principal of Gensler Architects, explained Gensler’s assignment: “Our assignment was to take this dilapidated, outdated mall and convert it into a 24-hour business/lifestyle environment that is a great place to work as well as a key attraction for San Fernando Valley residents.” The ambitious plan included redeveloping the retail-oriented Sherman Oaks Galleria into a 700,000 SF Class-A office project supported by a 300,000 SF outdoor lifestyle complex, which would include many restaurants, a new theater, a gym, a cosmetology school/salon, and many other uses.

Whereas the original Sherman Oaks Galleria was repeatedly criticized for its unwelcoming, closed-off design, the new design created the opposite effect. Gensler’s design would turn the Sherman Oaks Galleria into a predominantly outdoor lifestyle center with three pedestrian entrances: One from Sepulveda Blvd, one from the corner of Sepulveda and Ventura Blvd, and one from the parking structure. Each of the two sidewalk entrances lead to spacious plazas, both of which include pleasant water features. The majority of the new mall’s square footage are either surrounding these plazas or located along the promenade walkway which connects the two plazas. The experience is so well-created that most visitors probably don’t realize that the Sherman Oaks Galleria consists of 70% office space, with just 30% retail uses.

Douglas Emmett’s 2006 IPO prospectus contains a brief explanation of the redevelopment work, which is quoted below:

During the course of this redevelopment, we demolished a large portion of the mall and built a four-story structure containing lifestyle amenity retail uses as well as a new retail promenade. The balance of the mall space was converted to office space, and we also reconstructed an office building on the site. Additionally, the existing office tower was renovated to provide a new lobby with direct access to the retail promenade. As a result of this redevelopment, we transformed the property into a one million square foot, integrated mixed-use project, primarily consisting of office space enhanced by a high level of retail amenities.

Directory map of the updated Sherman Oaks Galleria

The Financials Behind the Galleria’s Renovation

The transformative renovation came with a hefty price tag. According to Douglas Emmett’s 2006 IPO prospectus, Douglas Emmett capitalized $199,649,000 of costs relating to the Sherman Oaks Galleria subsequent to its 1997 acquisition. Capitalized costs include design costs, construction costs, broker commissions, landlord contributions for tenant buildout, and many other costs required to stabilize a property which can’t be written off as expenses during the year the costs are incurred. Therefore, Douglas Emmett’s all-in costs for the stabilized Sherman Oaks Galleria including its $51 million initial acquisition price totaled approximately $250 million.

Isn’t a $200 million renovation a bit excessive? If spending $200/PSF on a renovation, why not just build an entirely new project? Because of Douglas Emmett’s deep involvement in the Sherman Oaks/Encino submarket (Douglas Emmett owned eight other office buildings in the submarket), the company had a deep understanding of not only the strength of office demand, but also the submarket’s supply restrictions. The idea of owning properties in supply-constrained markets is alluded to repeatedly in the prospectus and is at the core of Douglas Emmett’s investment philosophy as listed on its website. Douglas Emmett knew that due to the 1986 passing of Proposition U there were high barriers-to-entry for new development in the Sherman Oaks submarket. In fact, during the period between 1996 and 2006, the Sherman Oaks submarket experienced no new Class-A office deliveries besides the Sherman Oaks Galleria. By redeveloping the original Sherman Oaks Galleria primarily into a Class-A office building, Douglas Emmett would be granted entry into a club which had stopped accepting members fifteen years earlier: An exclusive club of Class-A office owners which would be experiencing outsized rental rate increases due to politically-created supply limitations. In a way, Douglas Emmett’s plan on building Class-A office space under the guise of the obsolete Sherman Oaks Galleria could be understood as the acquisition of a 300,000 SF existing office building (the existing Comerica bank building) with pre-approved entitlements for the construction of an additional 400,000 SF of Class-A office space and an additional 300,000 SF of retail space (the Lifestyle Building, the Courtyard Office Building, the Garden Office Building, and the Warner Bros building.)

Douglas Emmett’s strategy of investing in high barrier-to-entry markets was highly successful. At the time of Douglas Emmett’s acquisition, Douglas Emmett estimated market asking rents to be approximately $23.13/SF. By 2006, Douglas Emmett would be attaining average rents of $29.14/SF at the Galleria, with the Sherman Oak Galleria’s occupancy at 99.7%.

Estimating the Net Operating Income of the Sherman Oaks Galleria

- 2006 Annual Income Calculations:

- Gross Rental Income: 1,002,561 SF * $29.14/SF = $29,214,627

- Parking income (ParkMe.com): 3,425 parking spaces * 100/month = $4,110,000

- Total Estimated Income: $33,324,627

- Less 5% Vacancy: ($1,666,231)

- 2006 Income Estimates: $31,658,000

- 2006 Annual Expense Calculation

- Estimated Expenses: $12/SF * 1,002,561 = $12,030,000

- 2006 Annual NOI Calculation: ($31,658,000 – $12,030,000) = $19,628,000

Considering the Galleria’s location, quality, age, and property type, the property would likely be valued at a 5 capitalization rate, or stated another way, 20 times the property’s annual net operating income. Considering the property’s 2006 NOI of $19,628,000, the property’s 2006 value based on a 5% cap rate would be $392,560,000. Not bad, considering that Douglas Emmett’s acquisition costs of $51 million and its capital expenditures of approximately $200 million, total approximately $251 million.

As stated in Douglas Emmett’s 2006 IPO prospectus, the Sherman Oaks Galleria was encumbered by approximately $195 million of debt at a 5% interest rate with interest only payments (no amortization). The annual debt service (total amount of annual mortgage payments) amounts to $9,750,000.

Therefore, considering that in 2006 Douglas Emmett had approximately $55 million of its equity invested in the opportunity ($250 million total costs less $195 million loan amount), the cash-on-cash return could be calculated as follows:

- Net Operating Income = $19,628,000

- Less: Debt Service = ($9,750,000)

- Equals: Cash Flow = $9,878,000

- Equity Invested = $55,000,000

- Cash-on-cash return after refinance: ($9,878,000 / $55,000,000) = 17.96%

The Sherman Oaks Galleria: A model for other malls or an outlier?

At the time of this writing in early 2017, there is uncertainty regarding the long-term viability of thousands of malls across the country. These malls are being challenged by a combination of forces including the explosive growth of online shopping, the closure of many anchor stores, the closure of many inline shops, and outdated malls in dire need of capital-intensive renovations. For example, in just the first few weeks of 2017, Sears announced it would be closing 150 stores, Macy’s announced it would be closing 100 stores, and Limited Too announced it would be closing 250 stores. Each of these store closures, especially of the traffic-generating anchor stores, pose a significant threat to the regional malls in which they are located.

Unlike the Sherman Oaks Galleria, many of these malls are located in relatively lightly-populated markets with weaker market fundamentals than Sherman Oaks. Often times, lower market rental rates and property values mean that $200 million renovations aren’t financially viable. Faced with limited options and insurmountable challenges, many owners of non-viable, rural malls are giving up and handing their properties over to lenders. A recent Wall Street Journal article titled “Mall Owners Rush to Get Out of the Mall Business,” explains the recent challenges facing owners of enclosed shopping malls which is affecting even the most sophisticated and experienced mall owners. The article provides recent examples where elite mall owner such as Simon Property Group, Washington Prime Group, CBL & Associates Properties have voluntarily relinquished ownership of properties to lenders.

Although malls in primary markets are encountering the same headwinds, these malls are able to justify spending hundreds of millions of dollars on the major renovations. A renovation which doesn’t make financial sense in a mall where rental rates are $12/SF could pencil out just fine in a mall where annual rental rates exceed $100/SF.

Interestingly, almost all malls in West Los Angeles have recently undergone renovations or will soon undergo renovations. These renovations are not cosmetic, but rather monumental undertakings which change the strategy, atmosphere, and business models of the mall. Said renovations include Beverly Center’s $500 million in-progress renovation, Century City’s $800 million in-progress renovation, Santa Monica Place’s recently completed $265 million renovation, and Westside Pavilion’s major planned renovation, which will almost certainly come in at more than $100 million.

In light of the challenges facing regional malls, the successful repositioning of the Sherman Oaks Galleria offers some ideas and lessons which may be able to be applied to other struggling malls. Some of these general ideas include:

- Consider alternative/creative uses for all or part of the mall’s space. One of the keys to the successful repositioning of the Sherman Oaks was converting much of the mall to office space. By converting much of the mall’s square footage to office space, Douglas Emmett essentially reduced the size of the shopping mall and significantly reduced the supply of retail space. Likewise, owners of struggling malls should consider embracing unconventional uses for mall space. For example, malls could offer themselves to municipal uses (libraries, city hall, etc.), general office uses, medical uses, educational uses (trade schools, charter schools, universities, beauty schools), and gyms.

- Maximize tenant visibility and pedestrian traffic. One of the key outcomes of the Galleria’s renovation was that most of the tenants were located surrounding the open plazas or along the promenade connecting the two plazas. This layout ensured that most of the Galleria’s new businesses experienced sufficient visibility and sufficient foot traffic, rather than relying on anchor tenants for visitor traffic.

- Embrace entertainment-oriented, non-retail tenants. In light of the emerging dominance of e-commerce, customers no longer need to visit malls in order to shop. Rather, the new role of malls will be an entertaining environment which serves its customers through non-retail uses. Such uses include restaurants, movie theaters, gyms, beauty schools, nail salons, ice cream shops, coffee shops, and other similar uses.

Unfortunately, the future isn’t looking good for many of these rural malls. It will be interesting to see how/if these malls are redeveloped in the future.

Now, lets’s continue on to the some lessons and takeaways from Douglas Emmett’s acquisition and repositioning of the Sherman Oaks Galleria:

Lessons and Takeaways

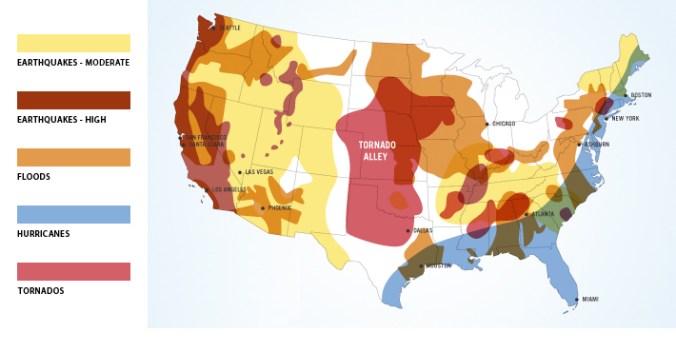

Lesson 1: Account for the likelihood of natural disasters

The Sherman Oaks Galleria’s challenges and downfall were greatly accelerated and exacerbated by the 1994 Northridge Earthquake. Are natural disasters just a general risk that real estate investors need to accept? Not necessarily. Although many people will dismiss natural disasters as “acts of God” and unpredictable, the reality is that many parts of the country are especially prone to natural disasters such as earthquakes, tsunamis, hurricanes, tornadoes, flooding, rising sea levels, etc.

Investors and homeowners would be wise to account for the risk of potential natural disasters and also the potential consequences of the natural disasters. Although the exact timing of earthquakes can’t be predicted, there is strong consensus about the causes of earthquakes and the time intervals at which certain faults rupture. For example, Southern California is especially prone to earthquakes. Considering that a portion of the San Andreas Fault hasn’t produced a large earthquake in over 159 years, there is consensus among scientists that there will be a major earthquake along that portion of the San Andreas fault in the near future.

To cite another example, there is a significant (and inevitable) risk of a large earthquake and tsunami in the Pacific Northwest region of the United States. The imminent earthquake and tsunami will likely destroy most of the older buildings in the region and cause billions of dollars of damage in the Pacific Northwest region.

USA Natural Disaster Risk Map

How should real estate investors act in light of the risk from natural disasters? At the least, investors should understand the risks of natural disasters and consider how their livelihoods will fare in a worst-case scenario case. For example, if an investor’s properties are all located in the Pacific Northwest, then a natural disaster in that region can devastate an investor’s livelihood. Even if an investor’s properties are insured, an investor may not have enough liquidity to cover the insurance deductibles, thereby rendering any insurance coverage useless.

One defensive step an investor can take is diversifying holdings across the different regions. For example, an investor that owns three assets in Seattle is much more susceptible to financial ruin at the time of the Cascadia Subduction Zone earthquake, than in investor who owns a property in Chicago, a second property in Seattle, and third property in Arizona.

Another option is for an investor to price the risk of natural disaster into an investor’s underwriting. For example, an investor who may have otherwise settled for a 10% return if a property is located in a non-disaster-prone area may require a 15% return for the same property located in a natural disaster-prone area.

Lesson 2: Unlike other property types, many retail properties are highly reliant on anchor tenants

Vacant mall anchor space

As real estate professionals, it’s important to fully understand the risks of investment opportunities. One of the risks present in larger retail properties (including malls), are the properties’ relatively high dependency on anchor tenants for the performance and success of the entire property.

For example, with regards to regional shopping malls, the departure/vacancy of an anchor tenant can often be a catastrophic event which can trigger a downward spiral. After the anchor tenant vacates their space, the remaining supporting tenants suffer due to lack of traffic, which can in turn decimate the mall owner’s net operating income and the shopping mall’s public perception. Making matters worse, many shopping mall leases include co-tenancy clauses, calling for reduced rents if the occupancy of the shopping mall falls below a certain level or if specified key tenants vacate their spaces. For these reasons, shopping malls carry additional risks which other property types aren’t as vulnerable to.

In the case of Galleria, the mere closure of the third floor of one of the mall’s two anchor spaces resulted in the closing of most of the third-floor’s smaller shops, which in turn resulted in the mall’s irreversible decline. Likewise, a grocery-anchored shopping center can suffer immensely with the vacating of the supermarket anchor space, which previously served as the shopping center’s main primary source of traffic.

Shopping malls’ reliance on one anchor tenant is greatly contrasted to other properties such as office buildings and apartment buildings. For example, if the occupancy of an office building or apartment building declines from 100% to 70%, the public’s perception of the property and the vitality of the property may not be negatively affected at all.

Therefore, it’s important for investors to understand and consider this additional area of risk for certain types of retail properties.

Lesson 3: Seek Off-market Acquisition Opportunities

Another lesson from Douglas Emmett’s acquisition of the Sherman Oaks Galleria is the idea of acquiring properties through off-market transactions. Most investors rely on online databases (Loopnet, MLS, etc.) to find acquisition opportunities. Often times, these widely marketed properties are either overpriced or, if not, are likely being pursued by dozens of other motivated buyers who are willing to acquire properties for a price close to or equal to market value. A few of the benefits of acquiring properties through off-market transactions are as follows:

- Less Competition: When acquiring off-market properties, an investor usually won’t be competing against any other buyers. For this reason, an investor can often negotiate more favorable price and terms.

- Direct Negotiations with Seller: Sellers of off-market properties are sometimes not as knowledgeable or up-to-date as listing brokers regarding market trends and property valuations

Lesson 4: The more scary/unique/challenged a property is, the better price it can usually be acquired at

One of the great aspects of real estate investing is the possibility of acquiring a property for less than market value and thereby earning an instant profit. However, acquiring properties significantly below market value is easier said than done because sellers and their brokers are usually well informed regarding a property’s value and potential.

Therefore, one of the only ways to acquire properties at an attractive price is to be willing to bear the risk and responsibility of acquiring properties which are challenged, risky, and unnerving to many investors. During the late 1990s, the Sherman Oaks Galleria was one such property. In 1997, the property’s occupancy was below 80% and the average rents were reduced to about 50% below market rents. The property was likely on the verge on unprofitability and there seemed to be no easy long-term fix to the Galleria’s problems. Most investors would likely dismiss an opportunity to acquire the Sherman Oaks Galleria as too risky or too capital intensive.

However, Douglas Emmett pursued this opportunity and was able to acquire the 1,000,000 SF building, 3,425 space parking garage, and 20-acre land parcel for just $51 million. Due to Douglas Emmett’s willingness to deal with the challenge, risk, and repositioning work, Douglas Emmett was able to acquire the property at a low price, and profit almost $150 million based on the property’s estimated 2006 value.

Lesson 5: Changing a property’s use can be an effective way of adding value to a property

At the time of Douglas Emmett’s acquisition of the Sherman Oaks Galleria, the property was attaining average rents of approximately $14.65/SF/year. Douglas Emmett realized that Class-A office rents in the area were approximately $23/SF/year, and noticed the potential profit that could be earned by renovating and partially rebuilding the property as a Class-A office property. The relatively high Class-A office rents would increase the value of the property significantly more than what the renovations would cost, thereby justifying the $200 million renovation project.

This strategy can also prove effective for smaller real estate projects. For example, in the last few decades there has been a trend in many urban areas where older high-rise office buildings have been converted to apartment buildings and condominiums. Through this repositioning strategy, an office building that would otherwise sell for $100/SF, could now be sold for $300/SF as residential condominiums.

Lesson 6: Specializing in specific property types and achieving market dominance can have major advantages

Since its inception, Douglas Emmett has abided by its calculated investment strategy of specializing in specific property types in specific submarkets. Specifically, Douglas Emmett specializes in Class-A office investments in Los Angeles and Honolulu. Over the years, Douglas Emmett has built up significant market shares of Class-A office space in these two areas.

As explained on Douglas Emmet’s website: “Once we select a submarket, we follow a disciplined acquisition strategy of gaining substantial market share to provide us with extensive local market information, pricing power in lease and vendor negotiations, economies of scale in property management, and an enhanced ability to identify and negotiate investment opportunities. In our target Los Angeles submarkets, we own on average about 27% of the Class-A office space; in Honolulu, we own and operate about 34% of the Central Business District Class-A office space.”

The strategy explained in the above quote clearly demonstrates one of Douglas Emmett’s long-time guiding investment principles of building up dominant market shares in just a few submarkets. Douglas Emmett’s 2006 IPO prospectus includes the below chart showing Douglas Emmett’s market share in the markets it invests in.

Chart showing Douglas Emmett’s market share in different markets

According to the above chart, as of June 30, 2006, Douglas Emmett owned and managed over 50% of the Class-A office space in the Sherman Oaks/Encino submarket. At the time of Douglas Emmett’s 1997 acquisition of the Sherman Oaks Galleria, Douglas Emmett already owned eight Class-A office buildings in the Sherman Oaks/Encino submarket where the Galleria was located. With Douglas Emmett’s unsurpassed market knowledge, economies of scale, and pricing power in the Sherman Oaks submarket, Douglas Emmett was able to confidently and boldly undertake the acquisition and repositioning of the Galleria. Through advantages offered by its dominant market share, Douglas Emmett significantly reduced its risk in undertaking the acquisition and repositioning of the Sherman Oaks Galleria.

Furthermore, Douglas Emmett continues to follow this strategy ten years later. After Douglas Emmett’s 2016 acquisition of four Westwood office buildings from Equity Office, Douglas Emmett secured a 74% market share of Class-A office space in the Westwood submarket.

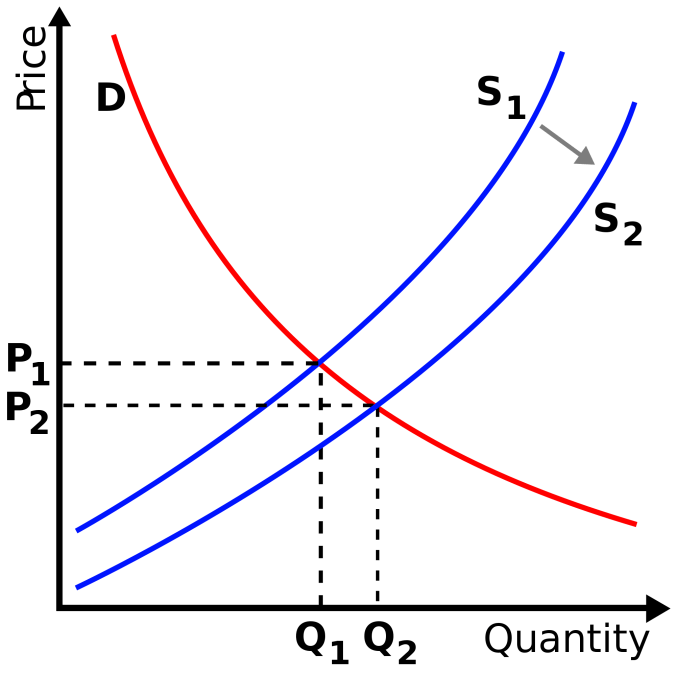

Lesson 7: Acquire properties in supply-constrained markets

Another key part of Douglas Emmett’s acquisition strategy is acquiring properties in supply-constrained markets. By acquiring and owning office buildings in markets with high barriers-to-entry, Douglas Emmett is in a position to benefit from rising rents resulting from the constrained supply.

Supply and Demand Curve

Let’s delve into why Douglas Emmett has decided on investing in Los Angeles and Honolulu. First off, both Los Angeles and Honolulu are supply-constrained for geographical reasons. Because Honolulu and Los Angeles are both coastal markets with mountainous terrain, developable land is more limited than in Oklahoma City or Kansas City, for example. In order to develop new high-rise office buildings (thereby adding supply to the Class-A office supply) in Honolulu or Los Angeles, developers often must acquire and demolish existing buildings. The costs associated with the acquisition, demolition, and new construction are often high enough to discourage developers from building new Class-A office buildings. As a result, supply is constrained and existing Class-A office building owners benefit from strong rent growth.

In addition to the physical supply constraints in Los Angeles and Honolulu, the supply in both markets is also constrained due to government-imposed development restrictions. Both markets are generally considered to be anti-development markets. Examples of development roadblocks include stringent environmental guidelines, voter-approved propositions, difficult city planning processes, and powerful anti-development homeowner groups. Douglas Emmett repeatedly alludes to the benefits of owning properties in such supply-constrained areas in its 2006 prospectus, one example of which is quoted below:

Each of our submarkets is generally characterized by supply constraints that are the result of down-zoning, economic constraints, restrictive planning commission practices and homeowner groups who are opposed to new development, all of which have created high barriers to the development of new office space. Proposition U, which was approved in 1986, decreased the development capacity of the City of Los Angeles by approximately 50% and affects the Brentwood, Olympic Corridor, Sherman Oaks/Encino and Westwood submarkets. Under the existing specific plans governing development within the Century City and Burbank submarkets, future development is extremely limited. The City of Santa Monica adopted a series of plans in the mid-1980s that imposed stringent limits on development in the downtown area where all of our Santa Monica properties are located, and Beverly Hills limits development through a discretionary approval process for virtually all new building.

All in all, Douglas Emmett was extremely strategic in building up its 17 million SF portfolio of Class-A office buildings. At least to some degree, Douglas Emmett’s acquisition strategy is guided by the basic economic principle of “supply and demand.”

Lesson 8: The revitalization of a major property in a market can boost surrounding property values. On the other hand, the decline of a major property can negatively affect surrounding property values

Another lesson from Douglas Emmett’s revitalization of the Sherman Oaks Galleria is an understanding of the effect that one real estate project can have on surrounding properties and possibly even an entire submarket. For example, in Douglas Emmet’s 2006 prospectus, Douglas Emmett briefly explained some of the benefits of the Galleria’s redevelopment: “We believe that the redeveloped Sherman Oaks Galleria supports and enhances the value of our other eight office properties in the Sherman Oaks/Encino submarket.” In other words, Douglas Emmett believes that renovated Galleria’s amenities as well as the boost in public perception following the Galleria’s revitalization, increased property values throughout the Sherman Oaks/Encino submarket.

On the other hand, an influential property’s decline can also negatively effect surrounding property values. For example, the thousands of declining malls throughout the country don’t just pose a threat to mall’s owners, but also may threaten the owners of the properties surrounding the declining malls. In a 2017 Wall Street Journal article regarding the challenges facing regional malls, Arthur Nelson, a professor of Urban Planning and Real Estate Development at the University of Arizona explains: “If a mall closes or goes into decline, you’re going to see declining property values in the area. The mall is a marker.”

As real estate professionals, we can benefit from this lesson in two ways: by acquiring properties in areas where new development or redevelopment is occurring or by exiting an investment upon noticing the first signs of a nearby major property’s decline.

More specifically, we can be prepared to benefit from the revitalization of surrounding properties by routinely researching and keeping up to date with development news, building/renovation permits, and neighborhoods that are in the path of development/redevelopment. Keeping up to date with these trends can provide investors with the information needed to acquire properties at the right time and “ride the wave” to higher property values.

On the other hand, investor can use their understanding of neighboring properties to protect their investments. For example, if the owner of a small retail building located near a shopping mall feels strongly that the JC Penney anchor store in the shopping mall will likely be vacating within the next few years, the owner of the small retail building may benefit by selling the small retail building before the mall’s predicted decline.

Thanks for reading the above blog post! We hope you found it enjoyable and educational. For updates on new blog posts, you can follow our blog and like our facebook page.

Also, Behind the Deals is seeking volunteer writers to research and analyze real estate deals. This could be a great opportunity for anyone that is passionate about real estate to learn about real estate investing, and most importantly a great way to give back to a community of both aspiring and experienced real estate professionals. Please email behindthedeals@gmail.com for more information.

Sources:

http://articles.latimes.com/1999/jan/28/business/fi-2431

http://articles.latimes.com/1998/jul/17/local/me-4583

http://articles.latimes.com/2001/feb/17/local/me-26565

http://www.wsj.com/articles/mall-owners-rush-to-get-out-of-the-mall-business-1485262801