Deal Summary

During 2004, New Pacific Realty Corporation (NPRC) acquired 8 acres of land underlying the Beverly Hills Robinson’s-May from Equitable Life Assurance Society for $33.5 million. At the time of the transaction, the 240,000 SF department store and accompanying 1,100- car parking structure that were situated on the 8-acre parcel were owned by May Department Stores, parent company of Robinson’s-May.

Constructed in 1952, the 240,000 SF department store opened for business as a Robinson’s department store. For the next 40 years, the building continued operating as a Robinson’s department store until Robinson’s merged with May Company California in 1993, at which time the store was rebranded as a Robinson’s-May department store.

Because the site was encumbered by Robinson’s-May’s long-term lease at a below-market rental rate (which meant that the landowner’s net operating income was significantly below market), New Pacific Realty was able to acquire the land for a fraction of what the land would be worth if it wasn’t encumbered by the long-term Robinson’s-May lease.

Approximately two years into New Pacific Realty’s ownership, Federated Department Stores (which has since been renamed Macy’s) and May Department Stores (parent company of Robinson’s-May) jointly announced that Federated would be acquiring May for $17 billion. Consequently, Federated would be shutting down dozens of Robinson’s-May stores, including the underperforming Beverly Hills location. During late 2005, Federated announced its intentions to terminate the lease of the Beverly Hills Robinson’s-May location, which would lead to the store’s eventual closing during March 2006.

Following the closing of the Beverly Hills Robinson’s-May and the terminating of Robinson’s-May’s lease on the 8-acre parcel, the 8-acre parcel was no longer encumbered by a long-term lease, which meant that New Pacific Realty could explore options of developing the land. Over the next year, New Pacific Realty worked with world-renowned architects Richard Meier & Partners to draft architectural plans for a 252-unit luxury condominium project.

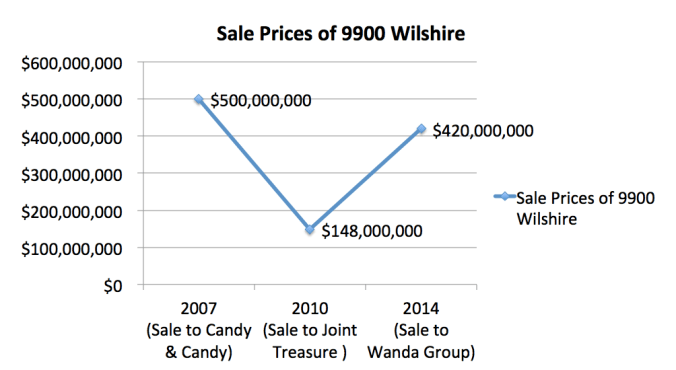

During 2007, New Pacific Realty sold the 8-acre parcel at 9900 Wilshire Blvd as a condominium development site to London-based developers Candy & Candy for $500 million. The sale would earn New Pacific Realty an estimated $450 million profit, just a few years following its 2004 acquisition of the 8-acre parcel for just $33.5 million.

During 2010, in the midst of the Great Recession, Candy & Candy lost the property to foreclosure. Shortly after the foreclosure, the lender conducted a private auction where the property sold to Joint Treasure International, an Asian real estate private equity firm, for $148 million, reflecting a discount of over 70% from the property’s 2007 selling price.

Eventually, during 2014 The Wanda Group acquired 9900 Wilshire Blvd for an estimated $420 million. Following its acquisition, The Wanda Group would rebrand the 252-unit condominium development as “One Beverly Hills,” while also working with the City to gain approval for a slightly modified mixed-use development which is now proposed to include a hotel component.

A Beverly Hills Icon: The Robinson’s-May Building

The Beverly Hills Robinson’s-May department store held its grand opening on February 13, 1952, originally branded as a Robinson’s Department Store. The 240,000 SF building was built to the highest standards at a cost of $6 million (not adjusted for inflation), complete with high-end finishes constructed with imported materials from around the world.

The building’s high-quality construction was appropriate for its flagship location and parcel, which consisted of approximately 8 acres of land overlooking the historic Los Angeles Country Club at the western entrance to Beverly Hills. Moreover, the newly-built Robinson’s was located adjacent to the Beverly Hilton Hotel which would be constructed just a few years later at the intersection of Santa Monica Boulevard and Wilshire Boulevard.

Early photo of the Beverly Hills Robinson’s Department Store

Early photo of the Beverly Hills Robinson’s Department Store

Early photo of the Beverly Hills Robinson’s Department Store

Aerial photo of the 8-acre parcel at 9900 Wilshire Blvd

As decades passed, sales revenues of the Beverly Hills Robinson’s store gradually declined. Many would attribute this decline to the prevalence of newer regional shopping malls throughout the country. Whereas department stores originally succeeded as standalone buildings, newer department stores were being positioned as anchor stores within regional shopping malls where all stores would benefit from the synergy and traffic provided by a complementary mix of dozens of retail stores. More specifically, the Robinson’s Department Store’s business was directly challenged by the 1964 opening of the nearby 900,000 SF Century Square Shopping Center, now known as Westfield Century City. The 900,000 SF Century Square Shopping Center included two department stores, which have now been rebranded as Bloomingdales and Macy’s. In part due to this major shift in the department store industry, Robinson’s exeprienced significant sales and traffic declines of its Beverly Hills location until the early 2000s.

Further compounding its challenges, since the Beverly Hills Robinson’s-May was located on land that was being leased by Robinson’s rather than owned by Robinson’s, Robinson’s was highly disincentivized from investing into major renovations of its aging, outdated building because it knew the building would eventually revert to the landowner when the lease would end. Thus, the delay of major renovations further contributed to the decreasing sales and traffic of the Beverly Hills Robinson’s-May store.

Due to the inevitable downward spiral caused by shifts in the department store industry and its outdated building, during the early 2000s it was estimated that the sales of the Beverly Hill’s Robinson’s-May were approximately 90% less than would have been expected for a flagship department store to operate viably. As real estate values skyrocketed during the early 2000s, the highly underutilized 8-acre parcel attracted the attention of many prominent real estate developers that each hoped to acquire a site widely considered to be one of the last remaining major development parcels in Beverly Hills.

Mid 2000s photo of the Beverly Hills Robinsons-May

New Pacific Realty Acquires the Underlying Land for $33.5 Million

The rise of New Pacific Realty is an inspiring story about two experienced real estate professionals, David Margulies and Arnold Rosenstein, who founded the investment company in 2002. Following successful careers spanning several decades and over 100 completed transactions, David and Arnold headquartered their new company in Beverly Hills. Within a year of its founding, New Pacific Realty completed its first high-profile deal with the 2004 acquisition and subsequent disposition of the Transamerica Center in Downtown Los Angeles.

In 2004, New Pacific Realty acquired its second high-profile property: the 8-acre parcel underlying the Beverly Hills Robinson’s-May from London-Based The Equitable Life Assurance Society for $33.5 million.

$33.5 million compounded for 30 years at 10% interest

Although the value of the raw land was significantly greater than $33.5 million, the sale price of the land was greatly diminished by the long-term Robinson’s-May lease which likely had at least 30 years remaining at a below-market rent which was likely well under $500,000 annually. Based on these estimated numbers, the owner of the land would be limited to a cap rate of less than 2% for over thirty years, before the owner would have an opportunity realize the full potential of the land. The difference between earning a 2% annual cash-on-cash return versus earning a 10% annual return is enormous, especially when compounded over 30 years.

To fully internalize the financial implications of this scenario, consider that if $33.5 million is compounded at an interest rate of 10% for 30 years, the future value at year 30 is almost $584 million. Therefore, considering the situation and based on this type of analysis, New Pacific Realty would be paying a much higher price by acquiring the 8-acre land for $33.5 million, because of the 30 years of annual income which it would be foregoing for the most part.

However, New Pacific Realty seemed to realize circumstances which could lead to a huge profit for themselves as the future landowners: both the existing landowner (Equitable Life Assurance Society) and the lessee (Robinson’s-May) were in less-than-ideal situations considering each of their objectives. These were issues which New Pacific Realty would be able to resolve, and which could be resolved in a manner which would create a win-win-win situation for all stakeholders including New Pacific Realty.

First off, as a life insurance company Equitable Life Assurance Society profits primarily through investing the annual premiums it receives from its life insurance policy holders, before it eventually pays out funds to its policy holders at a later date (essentially receiving a low-interest or possibly even interest-free loan from its policyholders, which it invests in order to earn its profit). Therefore, Equitable Life Assurance Society was primarily motivated to earn a reliable, high cash-on-cash return. Regardless of the long-term investment potential of the land underlying the Beverly Hills Robinson’s-May, the sub-2% annual yield was certainly not ideal from the perspective of a life insurance company.

Likewise, Robinson’s-May was facing its own challenges. By the early 2000s, the Beverly Hills Robinson’s-May building and parking structure were over 50 years old and in desperate need of a major renovation. Considering the enormous 240,000 SF building and 8-acre parcel size, a thorough, high-end renovation would likely require an investment of at least $50 million. However, due to the estimated 30-year remaining lease term (after which the landowner would almost certainly terminate the lease in order to develop the parcel to its full potential) and also due to the low historical revenues of the Beverly Hills Robinson’s-May, it was probably extremely difficult for Robinson’s-May to justify a $50 million renovation which would need to be fully amortized.

New Pacific Realty understood that it could help resolve Equitable Life Assurance Society’s situation by acquiring the 8-acre parcel for $33.5 million, which would enable the insurance company to reinvest the sales proceeds at a significantly higher cash-on-cash yield through more conventional real estate investments.

New Pacific Realty Finds a Creative Solution for Robinson’s-May’s Dilemma

Solving Robinson’s-May’s challenge would be a bit more complicated. Shortly after acquiring the property, New Pacific Realty approached Robinson’s-May and suggested that New Pacific Realty could redevelop the entire 8-acre parcel and incorporate a brand new flagship Robinson’s-May building into the proposed mixed-use development. For the next two years, discussions between New Pacific Realty and Robinson’s-May continued about the proposed mixed-use development.

Discussions between Robinson’s-May and New Pacific Realty halted when in July 2005 Federated Department Stores and May Department Stores (the parent company of Robinson’s-May) announced that Federated would be acquiring May in a $17 billion transaction. At the time of the announcement in 2005, Federated already operated two department stores in Westfield Century City within a few blocks of the Beverly Hills Robinson’s-May, and it likely wouldn’t need a third department store in the immediate area. A few months after the merger announcement, in November 2005 Federated announced it would be closing dozens of Robinson’s-May stores including the Beverly Hills location.

New Pacific Realty Creates a Vision for 9900 Wilshire

During the couple of years following Federated’s and May’s announcement, New Pacific Realty immediately started working toward developing the site. It hired world-renowned architects of the iconic Getty Center, Richard Meier & Partners, to design a mixed-use project. The proposed project would consist of 252 residential condominiums and a small retail component, with a total estimated construction cost of $500 million. The two 12-story towers on the site would be designed and built to LEED Gold standard, one of the most stringent environmentally-green designations for new buildings.

Site Plan of 9900 Wilshire

New Pacific Realty Sells 9900 Wilshire as a Development Site for $500 million

During April 2007, New Pacific Realty sold 9900 Wilshire to London-Based developers Nicholas and Christian Candy of Candy & Candy for $500 million in a transaction brokered by CBRE broker Laurie Lustig-Bower.

Candy & Candy funded the acquisition with a $135 million down payment and a $365 million short-term loan. For the most part, Candy & Candy planned on continuing the development process based on New Pacific Realty’s Richard Meier-designed project.

In an interview following its high-profile acquisition, Candy & Candy’s principal explained the company’s plans for the project: “We intend to see this vision through and bring Beverly Hills what will truly be the world’s most luxurious address… I believe this will be the One Hyde Park of the West Coast of America.”

How could Candy & Candy justify paying $500 million on land which it could build approximately 250 condominium units ($2 million land cost per proposed condominium unit)? In a 2007 article about the transaction, Candy & Candy reasoned that compared to real estate prices in London and New York City, real estate prices in Beverly Hills are relatively undervalued: “Everyone knows Fifth Avenue, Bond Street, and Rodeo Drive, but the prices are not comparable.”

To better understand Candy & Candy’s strategy, it helps to take a look at the company’s other developments. One of Candy & Candy’s best known developments is One Hyde Park, an 86-unit condominium development in London which has made headlines as one the most luxurious and pricey residential buildings in the world. Units in One Hyde Park have sold for up to 140 million pounds and are being marketed at approximately $10,000 per square foot, sales prices that can justify astronomical prices for development land as long as that land is suitable for an over-the-top development. The 8-acre development site located at 9900 Wilshire is one such site. Located a short walk from Rodeo Drive and with unobstructed views of the adjacent Los Angeles Country Club, Candy & Candy had reason to believe that a condominium development at 9900 Wilshire could achieve record-breaking sales prices. Commenting on the new buyer’s plans for 9900 Wilshire, Laurie Lustig-Bower, the real estate broker representing Candy & Candy in its acquisition of 9900 Wilshire explained, “Candy & Candy in the U.K. is what Tiffany is to jewelry here. Therefore they believe they will achieve record prices for their condos.”

Lender Forecloses on 9900 Wilshire During the Recession and Lender Sells 9900 Wilshire Via Private Auction

Barely a year following its acquisition of 9900 Wilshire and less than six months after plans for the project were approved by the city of Beverly Hills, during October 2008 a notice of default was filed by the project’s lender. The notice of default was the first step in a two-year process which would result in the property’s foreclosure and repossession by Banco Inbursa, a bank owned by Mexican Billionaire Carlos Slim.

Within a year following Candy & Candy’s 2007 acquisition, the real estate market had taken a sharp downward turn. Just a few weeks before the notice of default was filed, Candy & Candy’s investment partner in 9900 Wilshire, Iceland’s Kaupthing Bank, collapsed and was taken over by the Icelandic Government. Further compounding Candy & Candy’s troubles, the short-term $365 million loan which Candy & Candy planned to replace with construction financing, could no longer be replaced as the economy was now in a recession and construction financing was nearly impossible to come by.

The foreclosure process was completed in early 2010, and Banco Inbursa conducted a private auction for the sale of the property later that year. The private auction culminated in a winning bid of $148 million from Joint Treasure International Ltd, a Hong-Kong based real estate private equity firm specializing in acquiring “premier properties in premier locations.”

Joint Treasure International Ltd. held the property in its existing condition for about three years, before it was granted a demolition permit in June 2014, and subsequently proceeded to demolish the 62-year-old building and parking lot during July 2014.

Demolition of the former Robinson’s-May during July 2014

Joint Treasure International Sells 9900 Wilshire for $420 million

During mid-2014, Joint Treasure International listed 9900 Wilshire for sale with Laurie Lustig-Bower of CBRE, the same broker who brokered the property’s 2007 sale between New Pacific Realty Corporation and Candy & Candy. Lustig-Bower marketed the property as “an opportunity to develop a high-profile, entitled property located in one of the most recognizable cities in the world.”

During August 2014, Joint Treasure International Ltd finalized the sale of 9900 Wilshire to The Wanda Group for an amount reported by the LA Times to be $420 million. Wanda Group, the largest privately-owned real estate developer in the world, outbid 10 other investors in acquiring the opportunity.

Commenting on the completed sale, Thomas Liu of Joint Treasure International explained, “We never fall in love with real estate. When given the opportunity to build or sell outright, we chose the path of selling outright. We were very happy with our return.”

For the most part, The Wanda Group is planning on continuing to proceed with the approved Richard Meier plans from 2007. The major change implemented by The Wanda Group is replacing 5 floors of condominiums in the southern tower with 5 floors of hotel rooms which would have a private entrance from Santa Monica Blvd. According to The Wanda Group, the southern tower’s square footage and height will not be affected by the change of use.

Looking Ahead: 2017 and Beyond

Wanda Group’s project has been rebranded as One Beverly Hills, is scheduled for an early 2017 groundbreaking, and is projected to be completed by 2020. The development of One Beverly Hills is sure to be a fascinating ordeal in itself, filled with lessons and its own fascinating twists and turns. Anyone can guess whether or not One Beverly Hills will be profitable, but the uncertainties demonstrated through the following questions show that any opinion is just that:

- Will projected condominium sales surpass an average of $3,000/SF (a record-breaking price PSF for a condominium development in the Western United States)?

- Is there enough demand to absorb 250+ super-premium condominium residences?

- How long will it take to sell 250+ super-premium condominiums in Beverly Hills?

- How will the nationwide and global real estate sales market fare between 2017 and 2025?

- How will the nationwide and global real estate financing markets fare between 2017 and 2025?

- How will the cost of financing (interest rates) change between 2017 and 2025?

- How will the cost of construction (raw materials and labor) change between 2017 and 2025?

- How will the international economy fare between 2017 and 2025? (Including Middle Eastern economies, Asian economies, European economies, and the U.S. Economy)

- How much supply of super-premium condominiums will be entering the international market between 2017 and 2025?

Offering a bit of reassurance in the face of all the uncertainty, is that the Wanda Group is probably the developer that is best positioned to take on the risk of this development. Wanda Group is the largest privately-owned real estate developer in the world, and the Wanda Group is also a diversified conglomerate with business interests in wide-ranging sectors including children’s entertainment, tourism, sports, and film. Moreover, the Wanda Group’s business interests are diversified across dozens of countries on several continents. It will be interesting to see how both One Beverly Hills and the Wanda Group fare over the next 10 years.

Now, let’s move on to some lessons and takeaways:

Lessons and Takeaways

Lesson 1: When analyzing an investment opportunity, always consider (but don’t depend on) a parcel’s highest and best use

When analyzing a potential acquisition opportunity, one question to always consider is “what is the highest and best use of the property?” In other words, if the property was a vacant parcel of land, what would be the most profitable use of the property? If the acquisition opportunity is currently operating as its highest and best use, then the only path to profiting is through improving and maintaining the current operations of the property.

However, if the property isn’t operating as its highest and best use, then there may be a major potential profit now or sometime in the future through changing the property’s existing use to its highest and best use. For example, a property that is currently being used as a single family residence may have much more value if it can be used as multifamily development site. Or a property that is currently being used as a gas station may have more value as a development site for a mixed-use retail and apartment building. In the situation of the Beverly Hills Robinson’s-May, the highest and best use of the 8-acre parcel during 2007 was definitely not a standalone department store, but rather was likely a more profitable mixed-use project consisting of a combination of a hotel, residential condominiums, retail, and/or office. Because New Pacific Realty was marketing the property for sale based on its highest and best use, Candy & Candy had to pay for the property as if it was being sold as its highest and best use (a 252-unit condominium development site) rather than its existing use (a vacant 240,000 SF department store).

However, a property’s highest and best use is not always known to the current owners of a property. For example, a warehouse building may be worth $5,000,000 when valued based on its existing income as a warehouse building. However, the highest and best use of that property may be a multifamily development site, which may value the land itself at $10,000,000 and render the warehouse building to be valueless. If you can acquire a property without the seller knowing the highest and best use you can sometimes acquire a property at a fraction of its value. This example shows the importance of always considering the “highest and best use” of any property you’re analyzing, especially in urban locations where land is relatively limited.

It’s also important to note that a property’s highest and best use can change over time as a market’s supply/demand fundamentals change, land values change, new market trends emerge, and the uses of the properties surrounding a subject property change over time.

Steps to determine a property’s highest and best use

Lesson 2: Retail uses are highly dependent on synergy and traffic, and therefore benefit greatly from being located near other retail uses

One of the primary reasons for the low sales revenues of the Beverly Hills Robinson’s-May was the lack of retail businesses in the immediate area. The Robinson’s-May was bordered on its western side by the Los Angeles Country Club, on its eastern side by the Beverly Hilton, on its northern side by a residential neighborhood, and on its southern side by office buildings. Clearly absent from the Robinson’s-May’s immediate surroundings are any retail businesses which would have increased customer traffic to the Robinson’s-May. For example, a great way to understand synergy is to think about car dealerships which are usually located in close proximity to each other or outlet malls which consist of hundreds of off-priced clothing stores in close proximity to one another.

The lack of surrounding retail uses is greatly contrasted by Westfield Century City shopping mall, which consists of dozens of contiguous retail stores, each of which greatly benefits from the huge draw and foot traffic of the entire shopping mall.

Aerial rendering of Westfield Century City containing of dozens of retail stores totaling over 1 million SF

Likewise, the secluded location of the Beverly Hills Robinson’s-May is greatly contrasted to the location of the Beverly Hills Saks Fifth Avenue, which is located just steps away from the high-end retailers on Rodeo Drive, Beverly Drive, and Wilshire Blvd.

Lesson 3: Think about the implications of all of your actions/offers/decisions. New Pacific Realty may have saved tens of millions of dollars by offering Robinson’s-May a new retail store rather than a lump sum for a lease buyout

Upon acquiring the land underlying the Beverly Hills Robinson’s-May, most investors would immediately begin plotting on how they could unlock the full potential of the property by gaining control of the Robinson’s-May’s leasehold interest. In the case of the Beverly Hills Robinson’s-May, let’s consider New Pacific Realty’s 2004 purchase of the underlying land for $33.5 million. At the time of New Pacific Realty’s 2004 purchase, the land value of 9900 Wilshire (if it weren’t encumbered by the Robinson’s-May lease) would have been at least $150 million. Most investors finding themselves in New Pacific Realty’s situation would have approached Robinson’s-May and offered the retailer a lease buyout fee of up to $50 million in exchange for terminating the existing long-term lease. The investors would justify their offer to themselves by considering that they would be able to sell the land for $150 million and would have only invested a total of $83.5 million in the land, even after accounting for the enormous lease termination fee.

However, New Pacific Realty decided on a much wiser approach. Upon acquiring the property, New Pacific Realty approached Robinson’s-May and pitched Robinson’s-May on the opportunity to lease a newly-constructed department store which would be part of a new mixed-use development on the 8-acre parcel. Let’s go through the benefits of this creative, indirect approach:

- Through this indirect approach, Robinson’s-May management doesn’t internalize that their leasehold position is worth $50 million. If New Pacific Realty initially offered Robinson’s-May a $50 million cash buyout, then even if the buyout didn’t end up materializing Robinson’s-May would have forever felt entitled to a hefty cash buyout if they were to terminate their lease for any reason in the future

- As a retailer, Robinson’s-May was focused on increasing its store revenues and net operating profits. May was not focused on extracting real estate profits through creative real estate dealmaking. The proposed option for Robinson’s-May to occupy a newly-built flagship department store would have offered Robinson’s-May the opportunity to increase its store revenues, thereby achieving success through a metric that makes sense to Robinson’s-May upper management.

This indirect strategy ended up saving New Pacific Realty tens of millions of dollars in buyout costs when in 2005 Federated Department Stores and May Department Stores announced a $17 billion merger which would result in the voluntary closure of the Beverly Hills Robinson’s-May. If New Pacific Realty had offered Robinson’s-May a $50 million lease buyout two years earlier, then even if the buyout offer was rejected by Robinson’s-May, Robinson’s-May would still feel entitled to receiving a lump sum in exchange for terminating its lease, even if it would still otherwise plan on closing its Beverly Hills location. All in all, it’s important to consider the potential effects of actions which may initially seem simple and inconsequential. Take the time to think a few steps ahead and you’ll put yourself in a position to make wiser decisions.

Lesson 4: Think win-win and try to address other people’s problems/concerns

One of the greatest lessons from New Pacific Realty’s acquisition of 9900 Wilshire is how they were able to strategically and intelligently bring about the full potential of the property with the willing cooperation of all of the stakeholders directly and indirectly affected by the transaction. Let’s consider the perspectives of a few of the stakeholders:

- Equitable Life Assurance Society (Owner of Land until 2004)

- Goals:

- Earn the highest return possible (while taking on the least amount of risk) on its invested capital before that capital will eventually need to be paid back to life insurance policyholders

- Satisfying the Goal:

- At the time of New Pacific Realty’s acquisition, Equitable Life was earning a sub-2% annual cash yield on its investment for the remainder of Robinson’s-May’s lease term. By selling the land for $33.5 million, Equitable Life was now able to reinvest the sale proceeds into an investment which would likely provide an annual return of over 10%.

- Goals:

- May Department Stores (Long-term Lessee of Land)

- Goals:

- Increase revenues of its underperforming Beverly Hills location

- Satisfying the Goal:

- With less than 30 years remaining on its lease, May Department Stores was facing a situation where its aging, 50+ year old building was in dire need of a major renovation, but at the same time Robinson’s-May was having difficulty investing a large sum of money in a major renovation when it would lose possession of its building as soon as its lease ended. New Pacific Realty understood this dilemma and pitched May Department Stores on a scenario in which New Pacific Realty would redevelop the entire 8-acre parcel. The resulting new mixed-use development would include a newly-constructed Robinson’s-May location. This scenario would offer May Department Stores the opportunity to attract shoppers and increase revenues with a state-of-the-art, modern flagship store, while also retaining a long-term lease on the new location

- Goals:

- City of Beverly Hills

- Goals:

- Earn maximum tax revenues from the 9900 Wilshire parcel, while ensuring that the parcel is developed in a manner that will be beneficial to the city and its residents

- Satisfying the Goal:

- By redeveloping the highly underutilized site at 9900 Wilshire, the City of Beverly Hills would be achieving the goals of increasing property tax revenues, beautifying the western entrance of Beverly Hills, and further promoting Beverly Hills’ image as a high-end enclave.

- Goals:

By satisfying the goals of each of the stakeholders, New Pacific Realty was able to not only work toward gaining control of the entire opportunity (both land and building improvements), but was also able to receive preliminary approvals from the City of Beverly Hills to construct two-12 story towers with a total of over 250 units.

Lesson 5: Real estate cycles can lead to significant changes in real estate prices

The numerous sales of 9900 Wilshire provide a clear view of the vulnerability of real estate prices to real estate cycles. The property and development opportunity of 9900 Wilshire remained almost identical during the time between the 2007, 2010, and 2014 transactions. All three sales were marketed, sold and acquired based on nearly identical plans specifying an approximately 250-unit Richard Meier-designed residential condominium project. However, although the plans and project remained identical, the sales prices in the three transactions changed dramatically. In just three years between 2007 and 2010, the transaction price of 9900 Wilshire dropped over 70% (from $500 million to $148 million) due to the changes in the real estate market. In the 4 years following Joint Treasure International’s well-timed purchase, the sales price of 9900 Wilshire would almost triple from $148 million to $420 million.

It’s not always possible to perfectly time real estate cycles, but a good rule of thumb is to acquire properties during recessions and to sell properties when the real estate market is hot (supply is relatively low, demand is relatively high).

Lesson 6: Understand the risks of acquiring land for development

Acquiring land for development comes with many risks and disadvantages which investors should take into account when analyzing land acquisition opportunities. Many of these risks and challenges were experienced by Candy & Candy following their 2007 acquisition:

- Expect delayed returns: When acquiring land for development, an investor should take into account that they will not be earning a return on their investment for up to five years. The process of developing land can include multiple years of dealing with architects, governing bodies, contractors, lenders, and brokers before the investor experiences any cash return on their invested capital.

- Financing risk: Land acquisitions are especially prone to financing risk. As was the case with Candy & Candy’s acquisition, land acquisitions are often acquired with short term loans which investors plan on replacing with construction financing. However, relying on short-term loans is extremely risky, because construction financing can be very hard to come by during recessions and an investor can be left hanging without any backup options for refinancing the short term debt.

- Bearing the risk of assumptions: An investor acquiring land with the intention of developing is often making a long list of assumptions. For example, in acquiring 9900 Wilshire for $500 million, Candy & Candy justified its $500 million purchase by making assumptions relating to the prevalence of demand for super-premium residences, the price levels for super-premium condominiums, being able to obtain final approval for construction, construction costs, construction timeframes, interest rate levels, and much more. If those assumptions are too optimistic, an investor can be overpaying for land

- Land Prices are especially volatile: During recoveries and expansions, land prices usually increase more than other asset classes due to investor speculation and revised assumptions which usually encourage investors to pay much more for land based on slight changes in assumptions (For example, raising rental rate forecasts). Conversely, during recessions and contractions most investors turn away from land investing, and land sometimes drops in value by over 90% because development of land would no longer be profitable based on downward-revised forecasts. To fully understand the math behind the relatively large swings in land values, check out the following article which contains a concise explanation of the concept of land residual value: “Why land investment is so risky?“

The above risks are not deal-breakers in and of themselves. The major problem is that investors and developers often underestimate risks, and therefore settle for returns which don’t compensate them commensurate to the risk they’re taking on. Always consider all the risks of land acquisition, and compare the risks/rewards of land acquisition to the relatively less risky strategy of acquiring existing income-producing buildings.

Lesson 7: Know the market you’re investing in

History is full of examples where foreign real estate investors have significantly overpaid for United States commercial Real Estate. For example, such cases include Japan-based Shuwa Investment Corp.’s 1986 purchase of the Arco Plaza in Los Angeles for $640 million. After 17 years of ownership, Shuwa would sell Arco Plaza to Thomas Properties Group for just $270 million, a major loss which is even more dramatic when calculated in real terms due to 17 years of inflation. Many would also characterize Candy & Candy’s acquisition of 9900 Wilshire as another example of foreign investors overpaying for United States commercial real estate.

Such acquisitions by foreign investors can’t be wholly attributed to the swings of real estate cycles, but also have a lot to do with foreign investors not completely understanding the market they’re investing in. Supply/demand fundamentals, development processes/costs, demographic patterns, and economic situations all vary greatly between different international real estate markets. During the mid-to-late 1980s, when Japan was experiencing a major asset bubble and property prices were increasing exponentially, the idea of acquiring real estate in the relatively stable United States market seemed like a great idea. However, due to a lack of understanding of the intricacies of the United States real estate market, Shuwa Investment Corporation overpaid for Arco Plaza, and Arco Plaza would end up declining in value by over 80% in the few years following its acquisition.

Likewise, Candy & Candy’s misguided acquisition shouldn’t be solely attributed to the Great Recession, but should also be attributed to a lack of understanding of the local real estate market. In an interview immediately following its acquisition, Nick Candy of Candy & Candy commented on Beverly Hills real estate prices, “Everyone knows Fifth Avenue, Bond Street, and Rodeo Drive, but the prices are not comparable….I believe this will be the One Hyde Park of the West Coast of America.” In his statement, Nick Candy drew parallels between world-famous streets in New York City, London and Beverly Hills, implying that if condominiums in London are valued at up to $10,000 per square foot, then condominiums in Beverly Hills and Manhattan should also be valued at similar price levels. Also, by explaining 9900 Wilshire as the “One Hyde Park of the West Coast of America,” Candy provides a clear view of the thoughts that lead to investors overpaying based on misguided assumptions about real estate markets that are foreign to them. The problem with drawing parallels between different markets is that every market has its own intricacies including availability of land, costs of construction, development hurdles, etc.

Candy & Candy’s “One Hyde Park” Development in London

Instead of assuming that Beverly Hills was an undervalued market, a more risk-averse strategy may have been to consider historical sales data for condominiums in Los Angeles. An investor could then attempt to determine whether supply/demand fundamentals could support an additional 250 units of super-premium residences which would need to be sold at record-breaking prices in order for the development to be profitable.

Lesson 8: Creating plans for a development can increase a property’s selling price by demonstrating a parcel’s development potential

Soon after Federated Department Stores announced its acquisition of May Department stores, New Pacific Realty hired Richard Meier & Partners Architects to draft plans for a 252-unit luxury condominium project. Within a couple of years, 9900 Wilshire was transformed from an 8-acre parcel of land to a potential development opportunity for 252 super-premium condominium units.

When it came to marketing 9900 Wilshire for sale, New Pacific Realty was now selling an opportunity to construct a 252-unit iconic Richard Meier-designed condominium project. Each of the three subsequent owners of 9900 Wilshire apparently determined the 252-unit proposed development opportunity to be the ideal land use, as evidenced by each of the three buyers continuing to run with the plans after each of the property’s sales. Marketing the property together with building plans encourages potential purchasers to analyze the development opportunity based on the development that is proposed in the architectural plans. For example, Candy & Candy may have justified its $500 million acquisition as follows:

- Development Costs

- Land purchase price: $500 million

- + Est. Construction Costs ($500/PSF for 900,000 SF of building SF)=$450 million

- + Est Interest Expense during construction and holding: $300 million

- = Total development costs: $1.25 billion

- Total Profit Calculations:

- Condominium Sales: (750,000 net SF sold at $3,000/SF) = $2.25 billion

- Less: Sales costs: (6%* 2.25 billion) = $135 million

- Less: Total Development costs (calculated above) = $1.25 billion

- Total Profit: $865million

Based on the above calculations, Candy & Candy could have easily justified its $500 million purchase using the ambitious vision put forward in New Pacific Realty’s 252-unit Richard Meier-designed project. After paying $500 million for the land and accounting for all development costs, Candy & Candy could have projected earning $865 million in net profit through developing the property based on the architectural plans provided by New Pacific Realty.

On the other hand, if New Pacific Realty simply marketed 9900 Wilshire as “8 acres of land for development,” developers would strive to estimate the land value based on comparable land sales in Beverly Hills. They would logically think: “Why should I pay over $60 million per acre (over $1,000 per square foot) for 9900 Wilshire if the last three vacant land sales in Beverly Hills sold for an average $500/SF?”

All in all, drafting plans for a vacant land property can be a useful way for landowners to market a property based on its highest and best use. For example, if an investor owns a single story home situated on a parcel on which a 4-unit apartment building can be built, it might be worthwhile for the investor to hire an architect to design plans for a 4-unit apartment building even if the investor doesn’t plan on constructing the apartment building. By simply marketing the existing home together with the architectural renderings, an investor can guide the buyer’s thinking/analysis and demonstrate the full potential of the existing single family home.

Thanks for taking the time to read this article. We hope you enjoyed it and found the content interesting and educational.

Sources:

http://la.curbed.com/2010/2/5/10521736/candy-brothers-beverly-hills-site-heading-to-auction-block

http://www.wsj.com/articles/SB122532158922982061

Click to access 7EBC5FC79B69412E980FA0268A975514.pdf

http://www.costar.com/News/Article/Wanda-Group-Announces-$12B-Beverly-Hills-Mixed-Use-Project/163125

http://www.latimes.com/business/realestate/la-fi-robinsons-asian-investors-20140912-story.html

http://www.costar.com/News/Article/Wanda-Group-Announces-$12B-Beverly-Hills-Mixed-Use-Project/163125

http://www.latimes.com/local/la-hm-lostla14-2009mar14-story.html